AI's Biggest Constraint for Scale

The Void of Limited Energy

Disclaimer: This is not financial advice. The following article is a reflection of my own research, thoughts, and opinions. It is for informational and entertainment purposes only. Investing in stocks, startups, or any asset class involves risk. You should always conduct your own extensive research before making any investment decisions.

The story we tell about artificial intelligence is tidy: the cleverest model wins. In practice, the scarce input is not talent or silicon.

It’s electricity.

The limit on AI is measured in megawatts, not model weights. Once you accept that, the map of winners changes.

Start with economics, not evangelism. Generative AI breaks the old software rule that marginal cost trends to zero. Each prompt consumes compute and power. As models get larger and inference denser, the kilowatt-hours per query rise, not fall. That makes scale a double-edged sword. More usage can deepen losses if pricing doesn’t keep pace with energy and depreciation. The headline revenues are real; the operating leverage is not.

The result is a market where valuations rest on narratives while cash burn rises with engagement. That is not an accounting quirk. It is the business model.

The last time markets fell in love with a general-purpose technology, they made the same mistake. The late-1990s internet boom priced stories, not constraints. When it broke, the technology didn’t disappear; the value migrated to infrastructure. Logistics, broadband, payments and server capacity became the durable assets.

Nvidia plays Cisco to AI’s dot-coms. But even that analogy stops one layer too high. GPUs are a derivative good. Without cheap, reliable power, they sit idle. The true “picks and shovels” are turbines, substations and high-voltage lines.

The consumption profile is unambiguous. Data-centre demand is set to surge through the decade; AI is the driver. A single generative query draws several times the electricity of a standard search. Training runs that once sounded extravagant now look modest next to the gigawatt campuses on the drawing board. Flagship sites will require power on the scale of municipal baseloads. This is not a cloud. It is industry.

Now set that appetite against the grid we actually have. Utilities plan on decade horizons. Interconnection queues are long. Transformer lead times have stretched. In some hubs, developers are being told to expect multi-year waits for substantial connections. The clocks do not align: you can stand up a data hall in under two years; you might wait twice as long for power. Add intermittency. Wind and solar are essential, but 24/7 inference cannot follow the weather without storage or firm generation. Both remain constrained. Of the classic inputs (talent, data, compute, energy) the first three are elastic.

Energy is not. That makes it the binding constraint.

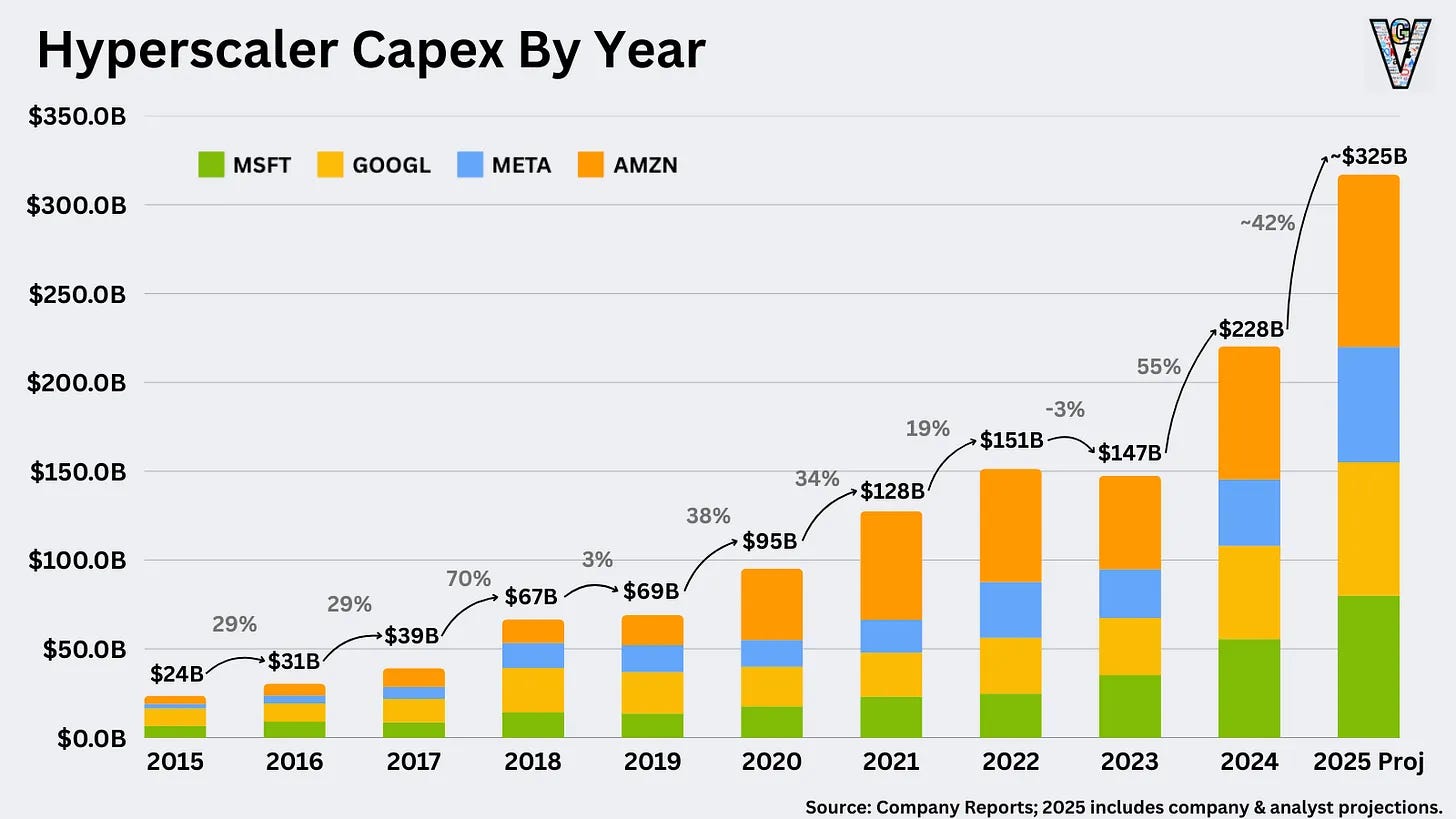

Yet the sector is pressing ahead with one of the largest capex cycles in corporate history. Hyperscalers will spend hundreds of billions on AI infrastructure this year, with more to come.

The logic is simple: spend or be left behind. History is less generous. Industries rarely earn excess returns by outbuilding one another. Capacity begets competition, and the gains leak to customers and suppliers.

In AI, the supplier with real scarcity is the power system.

The risk is clear: without secured, low-cost electricity, those beautifully engineered campuses become stranded assets. The second risk is subtler: if software and hardware progress bend the efficiency curve faster than expected, some hyper-specialised sites may be mis-sized or mis-located before their depreciation runs out. The telecom industry has seen this movie.

Geopolitics will reinforce the split. The US has focused on denying China access to top-end chips. China has focused on building energy. It has added renewables at extraordinary pace, advanced nuclear construction and secured control across key clean-energy supply chains and minerals processing.

It has also bought influence in foreign grids. In an AI economy, power-rich nations export computation much as oil-rich nations exported barrels. Power-poor nations import it—or curtail ambition. The leverage sits with those who can deliver firm, affordable electricity at scale. Chips matter. Power decides.

The industrial response is already taking shape. The archetypal winner is no longer a pure software firm. It is an energy-integrated operator. The most pragmatic players are co-locating compute with stranded or underused supply, signing long-dated PPAs, investing in storage and on-site generation, and designing workloads around the physics of electrons.

Every cent cut from delivered cost per kWh drops straight into gross margin on inference. Every extra “nine” of uptime you control becomes product. In a market where cost of goods sold is power plus depreciation on power-hungry equipment, the moat is physical.

Founders who treat power as a first-order product input will look conservative now and prescient later. Pick sites for time-to-power, not just tax incentives. Hire utility lawyers and grid engineers alongside ML researchers. Negotiate interconnections early and treat them as assets. Build energy-aware models and product features that price in kilowatt-hours, not only latency. Move computation to power rather than power to computation wherever possible. This is not romance for infrastructure. It is risk control and price discipline.

Investors should adjust their exposure accordingly. If you want AI’s durable cash flows, own what constrains and prices the cycle. That includes regulated utilities in bottlenecked regions, independent power producers with dispatchable assets near hyperscale clusters, transmission owners with credible projects through congested corridors and manufacturers of high-voltage equipment with backlogs that run for years. The new hybrids—firms that own generation, storage and compute under one roof—deserve serious attention. They will not screen as “software.” They will print operating leverage when others discover that token growth doesn’t pay the power bill.

There is a credible counter: efficiency will save us. Smaller, smarter models and better accelerators will cut energy per task. Good. They should. But technology rarely reduces total energy use; it reallocates it. Cheaper inference creates new demand, new products and new always-on workloads. The staircase pattern persists: step-changes in efficiency are followed by step-ups in total consumption. Scarce, expensive power slows adoption or pushes it to friendlier grids. Abundant, cheap power accelerates it. Either way, the determinant is kilowatts.

There is also politics. Communities tolerate data centres and new lines only if they share the upside. Permitting has become a shadow price. Firms that ignore local economics will discover the hard way that paperwork is a form of rationing. The fix is practical: credible community benefits, transparent water and power footprints, and visible investment in local reliability. It is cheaper than delays.

The most useful discipline now is to invert the usual questions. Don’t ask a model builder for parameter counts. Ask for a megawatt roadmap: secured supply, delivered cost, time-to-power. Don’t cheer capex without proof of electricity. Don’t underwrite multi-gigawatt campuses that rely on hypothetical grid upgrades. Price equity on energy strategy as much as product strategy. Reward firms that close the loop between electrons and tokens.

This is the uncomfortable conclusion. AI is not a software story with a utility footnote. It is an electricity story with a software interface. The winners will convert power into intelligence at the lowest, most predictable cost, in places where supply is secure and expandable. That favours owners of generation and wires, and it favours technology companies willing to become energy companies—by contract, by partnership or by outright ownership.

The market will catch up after it pays for its optimism. It always does. For now, the edge sits with anyone who can read an interconnection queue as easily as a model card. The kilowatt ceiling is real. Raise it, and you own the slope of AI’s growth. Ignore it, and you are renting your future from the people who don’t.